This week kicked off with strength in the markets as investors shrugged off last week’s derisking. Monday’s rebound was fueled by “buy-the-invasion” sentiment, and equities rose approximately 1%. Yesterday, the rally continued, helped along by a ceasefire agreement between Israel and Iran and a closely watched testimony from Federal Reserve Chair Jerome Powell.

But beneath the headlines lies a deeper story: a disconnect between Fed policy and what the data—and markets—are telling us.

Powell’s Testimony: A Key Shift?

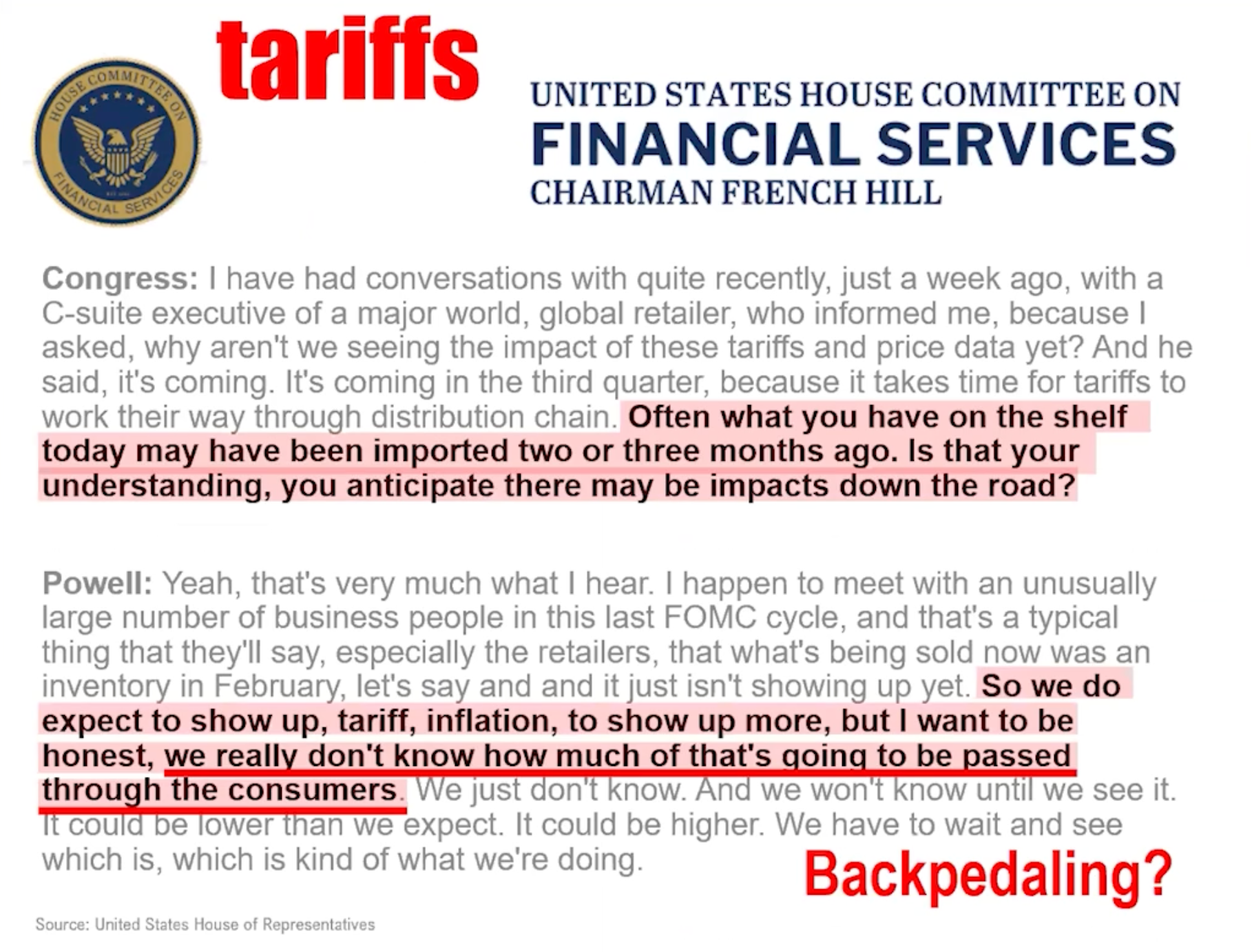

Speaking before the House Financial Services Committee, Chair Powell acknowledged that the Fed would likely still be cutting interest rates—if not for the inflationary expectations driven by tariffs.

“If it weren’t for higher inflation expectations from tariffs, we would have continued cutting rates.”THAT'S A BIG STATEMENT.

He went on to admit the central bank still doesn’t know how much of the tariff-driven cost increases will actually be passed along to consumers. That uncertainty, coupled with the Fed’s visible caution, had a dovish undertone—and the market noticed.

The Tariff Misunderstanding

Let’s unpack something important: tariffs aren’t classic inflation. They're a form of taxation. Whether the U.S. government raises $200 billion through traditional taxes or collects that amount via tariffs, it’s still a tax on consumption—not a true expansion of the money supply or cost-push inflation.

In fact, if businesses raise prices only to remit that money to the government via tariffs, that weakens consumer demand—not fuels inflation. The Fed typically views tax increases as disinflationary. So why are tariffs treated differently?

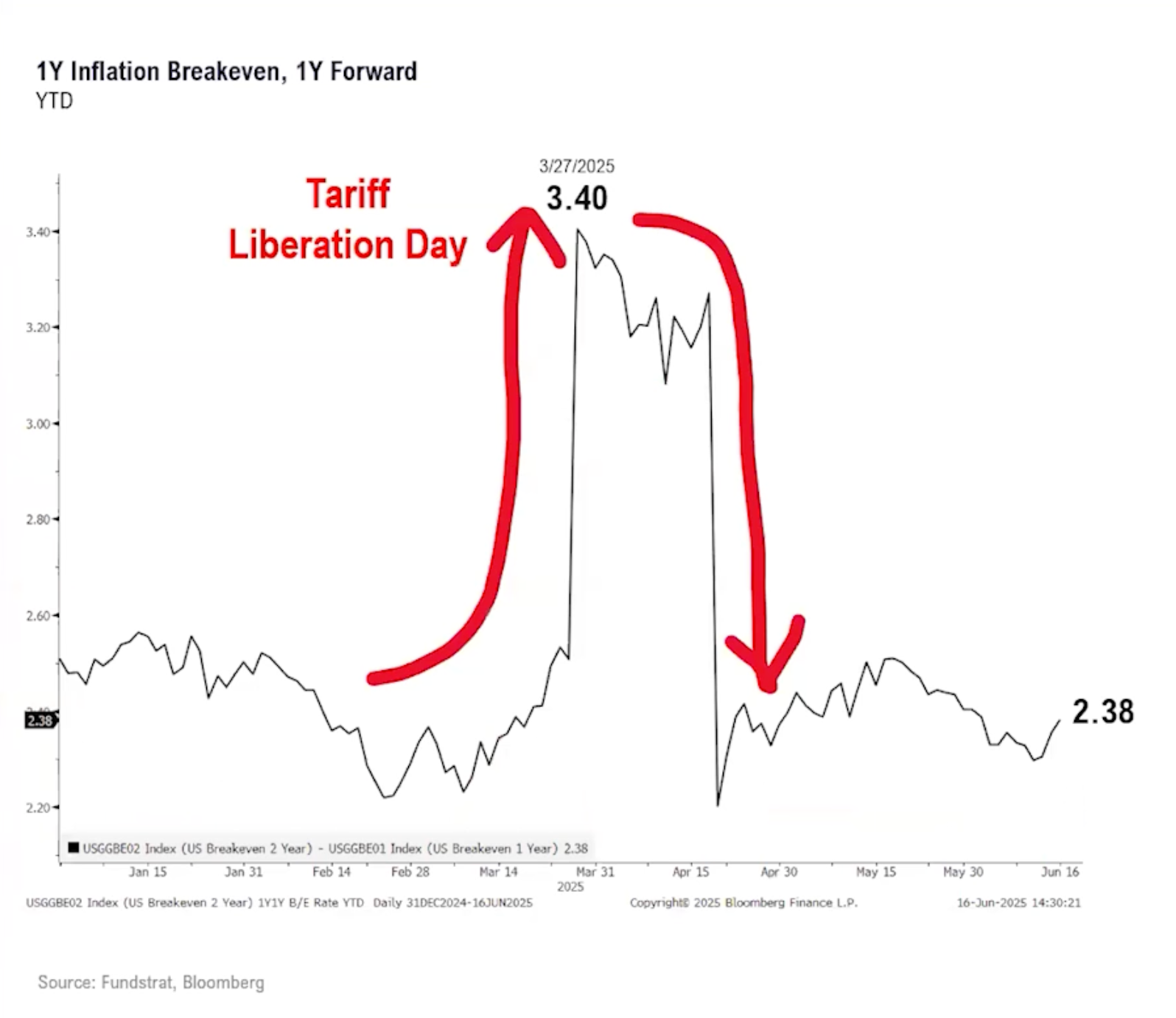

The bond market appears to agree with this logic:

- 1-year forward inflation expectations have dropped to 2.3%, below levels seen earlier this year.

- Consumer inflation expectations, per the Conference Board, have fallen from 6.0% to 4.9% in just two months.

This signals that both institutional and retail investors aren’t buying the idea that tariffs will drive sustained inflation.

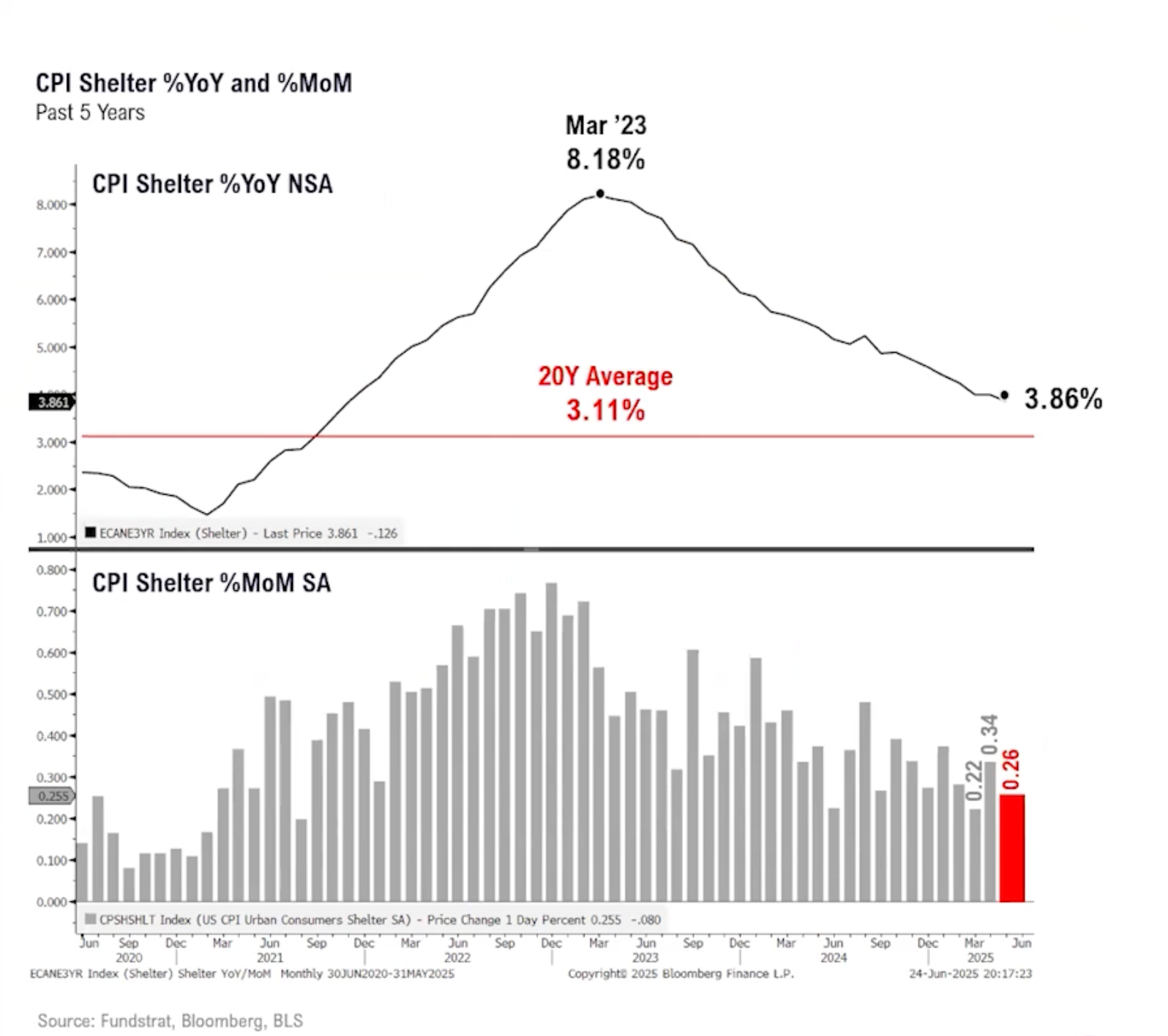

Is Housing the Real Target?

So why are rates still high?

One possible reason: housing. Powell knows current rates are hurting housing affordability, and shelter inflation has been one of the stickiest parts of the CPI. But that’s already correcting on its own. Housing is in a downcycle, and additional pressure may not be necessary—or productive.

What’s Next?

Powell speaks again tomorrow before the Senate. Then on Friday, we’ll get key readings from the University of Michigan sentiment survey and the Fed’s preferred inflation gauge: core PCE.

Still, even amid all this uncertainty, hedge funds are piling into short positions—now at the highest level since the start of 2024. It’s yet another sign this may be the most hated V-shaped rally we’ve seen in years.

The views stated in this letter are not necessarily the opinion of Cetera Advisors LLC. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed.